U.S. Exhibitions Industry Continues Strong Rebound, According to CEIR 2022 Fourth Quarter Index Results

April 11, 2023

The U.S. B2B exhibitions industry is continuing a robust rebound and demonstrating a continued improvement in Q4 2022 from the previous 11 quarters, according to the Center for Exhibition Industry Research’s (CEIR) 2022 Fourth Quarter Index results, which was released in late March.

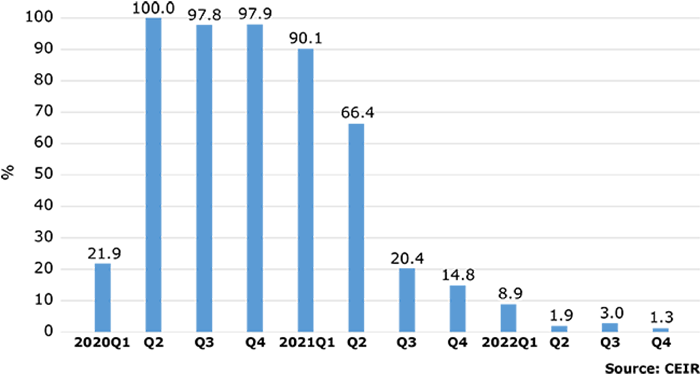

Figure 1: B2B Exhibition Industry Cancellation Rate, %

The cancellation rate for in-person trade shows and events dropped to 1.3%, a substantial improvement compared to 97.9% in Q4 2020 and 14.8% in Q4 2021. This relatively low cancellation rate and the continued improvement in metrics outcomes for completed events boosted the Q4 2022 Index result, according to CEIR officials.

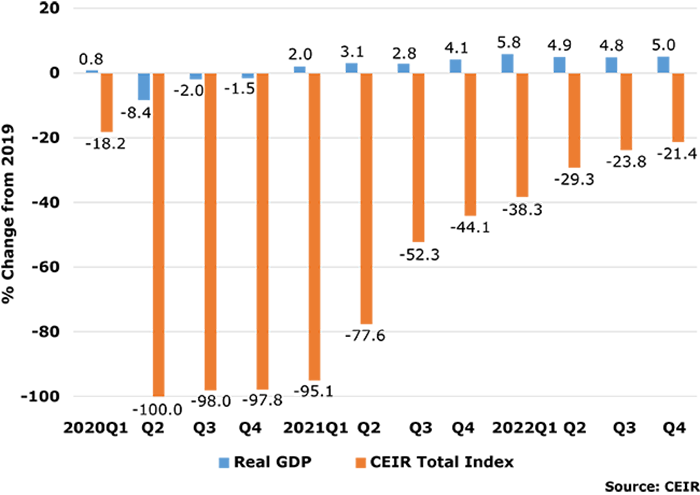

As expected, the CEIR Total Index, which is a measure of overall exhibition performance, continues to recover, surging 40.6% from a year ago. Compared to Q4 2019, it was still 21.4% lower (as shown in figure 2, below), nonetheless, this is a vast improvement compared to the past two years, which included declines of 97.8% from 2019 in Q4 2020 and 44.1% from 2019 in Q4 2021.

U.S. GDP and the CEIR Total Index

The U.S. economy’s performance was far better, registering a 5.0% increase in real (inflation-adjusted) GDP from Q4 2019 to Q4 2022. On a seasonally-adjusted annual rate (SAAR) basis, after two consecutive quarters of decline in Q1 and Q2, real GDP rose at a moderate rate, gaining 3.2% in Q3 and 2.6% in Q4. The rebound in Q4 primarily reflected increases in private inventory investment, consumer spending, nonresidential fixed investment, government spending at all levels and declines in imports that were partly offset by decreases in residential fixed investment and exports, according to CEIR officials.

Up to Q4 2021, economic recovery had been led by strong spending on goods, however, the initially sluggish recovery in services industries has recently continued to pick up the pace. In Q3 2021, real spending on consumer services finally recovered pandemic losses and robust expansion has continued since then. In Q4 2022, real spending on consumer services exceeded Q4 2019 spending levels by 4.2%.

Figure 2: Real GDP vs. CEIR Total Index, Q1 2020-Q4 2022, Percentage Change from 2019

Q4 2022 Exhibitions Industry Performance

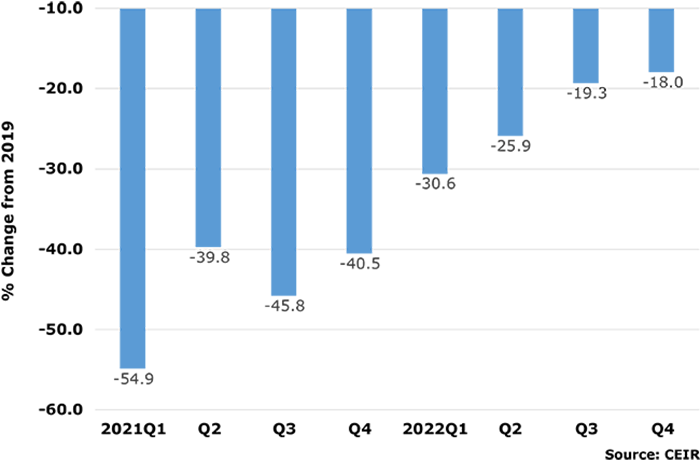

Figure 3 provides insights about events completed during Q1 2021 to Q4 2022, comparing the performance of each to the same quarter in 2019. While the Q4 2022 results demonstrate a continuing but choppy and uneven recovery underway, the direction is positive, with the overall Index and specific metrics improving for the past seven quarters.

Among completed events, 23.6% have surpassed their pre-pandemic levels of the CEIR Total Index. Some show organizers launched new shows, expanded existing shows to new locations or held them at a different time of the year. When looking at results excluding cancellations, the performance of events that took place in Q4 2022 demonstrates continued improvement, down only 18% compared to 2019 (Figure 3), a vast improvement compared to the decline of 54.9% registered in Q1 2021 compared to 2019.

Figure 3: CEIR Total Index Excluding Cancellations, Percentage Change from 2019

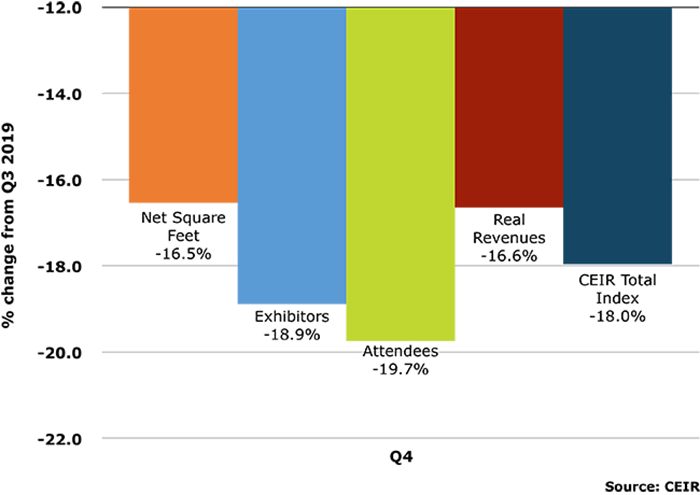

Among the four metrics (Attendees, Exhibitors, Real Revenues and Net Square Feet), Attendees has shown the least recovery, still 19.7% below results registered in Q4 2019, followed by Exhibitors with a decline of 18.9%. Real Revenues is 16.6% below Q4 2019, while Net Square Feet (NSF) in Q4 contracted the least at 16.5% from Q4 2019.

Figure 4: Q4 2022 CEIR Metrics for the Overall Exhibition Industry Excluding Cancellations, Percentage Change from Q4 2019

Insights on a Recession

The probability of a recession in 2023 stood at about 50% and now is slightly higher at 55% since the Silicon Valley Bank and Signature Bank of New York failures. The potential causes of a recession include tighter financial and credit conditions, a self-fulling prophecy and some unknown and unpredictable shocks. Businesses anticipating a recession ahead are cutting back their expenses and head counts. However, if there is a recession, it likely will be shallow for the following reasons:

- Household debt service payments as a percent of disposable income remains low even though it has inched up recently.

- There is pent-up consumer demand for services such as travel and tourism.

- Most large corporations still are flush with cash.

- There is a race to adopt new technologies such as artificial intelligence (AI) and electric vehicles (EV).

B2B Exhibitions Recovery

While 2023 is projected to be challenging for the exhibition industry as the economy slows down further and businesses are more cautious, the positive momentum of participation in face-to-face trade shows will continue, according to CEIR officials.

“The B2B exhibition cancellation rate should remain extremely low, and the performance of completed events will continue to improve,” said CEIR Economist Dr. Allen Shaw, chief economist for Global Economic Consulting Associates. “A full recovery for the industry is expected in 2024.”

Among the 14 industry sectors that CEIR monitors, the government and discretionary consumer goods and services sectors are expected to perform better, whereas the IT and building and construction sectors will lag behind the overall exhibition industry.

In late May, CEIR expects to release its 2023 CEIR Index Report, which analyzes the 2022 exhibition industry performance and provides an economic and exhibition industry outlook for the next three years, according to CEIR officials.

CEIR collects data directly from B2B exhibition organizers, who are encouraged to provide their show data by using the Event Performance Analyzer. In exchange for submitting valid B2B exhibition data, participants are provided with this tool that enables organizers to instantly see how an event’s performance compares to CEIR Index benchmarks at no cost. Data submission is strictly confidential, and the annual CEIR Index Report for their shows’ market sector is also provided to participating organizers at no cost.

Explanation and Definitions of Q4 Comparisons

As explained above, 14.8% of trade shows scheduled to be held in the fourth quarter of 2021 were canceled, limiting the usefulness of comparisons of Q4 2021 and Q4 2022 results, as any positive change would be very large and misleading. A more useful comparison is to the 2019 performance results, measured as the industry benchmark before COVID-19 forced the industry’s shutdown. Thus, events in the fourth quarter of 2022 are compared with those in the fourth quarter of 2019 in Figures 2-4. The CEIR Total Index in Figure 2 is a weighted average that includes both canceled events, with zero values for all exhibition metrics, and completed events. The Total Index in Figure 3 and Figure 4 exclude canceled events.

“Despite Omicron at the outset of 2022, CEIR research has documented an intent to return to face-to-face engagement at B2B exhibitions, and CEIR Index quarterly results continue to document the recovery is in progress,” said CEIR CEO Cathy Breden. “Each quarter, the Index is showing that more business professionals and exhibitors are coming back to the B2B exhibitions channel to meet their marketing, sales and business information needs.”

Don’t miss any event-related news: Sign up for our weekly e-newsletter HERE, listen to our latest podcast HERE and engage with us on Twitter, Facebook and LinkedIn!

Partner Voices

Overview:

The award-winning Orange County Convention Center (OCCC) goes the extra mile to make every day extraordinary by offering customer service excellence and industry-leading partnerships. From their dedicated in-house Rigging team to their robust Exhibitor Services, The Center of Hospitality brings your imagination to life by helping you host unforgettable meetings and events. With more than 2 million square feet of exhibit space, world-class services and a dream destination, we are committed to making even the most ambitious conventions a reality.

In October 2023, the Orange County Board of County Commissioners voted to approve allocating Tourist Development Tax funding for the $560 million Phase 5A completion of the OCCC. The Convention Way Grand Concourse project will include enhancements to the North-South Building, featuring an additional 60,000 square feet of meeting space, an 80,000- square-foot ballroom and new entry to the North-South Building along Convention Way.

“We are thrilled to begin work on completing our North-South Building which will allow us to meet the growing needs of our clients,” said OCCC Executive Director Mark Tester. “As an economic driver for the community, this project will provide the Center with connectivity and meeting space to host more events and continue to infuse the local economy with new money and expanding business opportunities.”

Amenities:

The Center of Hospitality goes above and beyond by offering world-class customer service and industry-leading partnerships. From the largest convention center Wi-Fi network to custom LAN/WAN design, the Center takes pride in enhancing exhibitor and customer experience.

The OCCC is the exclusive provider of electricity (24-hour power at no additional cost), aerial rigging and lighting, water, natural gas and propane, compressed air, and cable TV services. Convenience

The Center is at the epicenter of the destination, with an abundance of hotels, restaurants, and attractions within walking distance. Pedestrian bridges connect both buildings to more than 5,200 rooms and is within a 15-minute drive from the Orlando International Airport. The convenience of the location goes hand-in-hand with top notch service to help meet an event’s every need.

Gold Key Members

The OCCC’s Gold Key Members represent the best of the best when it comes to exceptional service and exclusive benefits for clients, exhibitors and guests. The Center’s Gold Key memberships with Universal Orlando Resort, SeaWorld Orlando and Walt Disney World greatly enhance meeting planner and attendee experiences offering world-renowned venues, immersive experiences and creative resources for their events.

OCCC Events:

This fiscal year, the OCCC is projected to host 168 events, 1.7 million attendees, and $2.9 billion in economic impact.

The Center’s top five events during their 2022-2023 fiscal year included:

AAU Jr. National Volleyball Championships 2023

200,000 Attendees

$257 Million in Economic Impact

MEGACON 2023

160,000 Attendees

$205 Million in Economic Impact

Open Championship Series 2023

69,500 Attendees

$89 Million in Economic Impact

Sunshine Classic 2023

42,000 Attendees

$54 Million in Economic Impact

Premiere Orlando 2023

42,000 Attendees

$108 Million in Economic Impact

Add new comment